Market Intelligence

The Atlanta Fed 3rd Q GDP number edged up to 1.4%.It was reported on Friday. It does not include the Employment Report. The next change will be August 10th. The Blue chip consensus is at 1.2%.So far no one has changed the forecast. Many have negative quarters ahead.

Next week will be interesting. I expect a number of economic forecast increases. On the other hand it is difficult to make high confidence changes on one report.

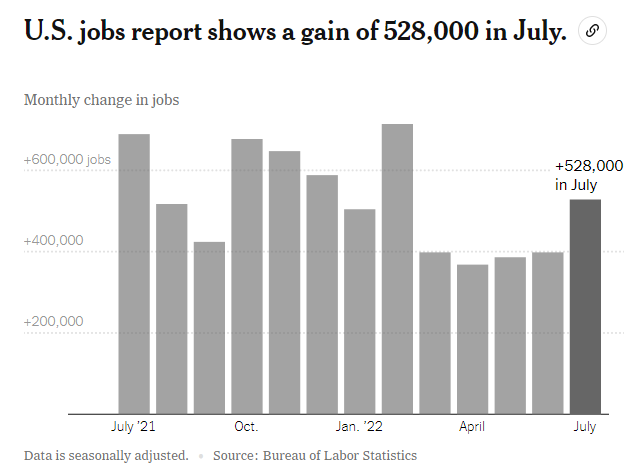

I suspect the seasonal adjustment exaggerated the report. The adjustment heavily weights the most recent months in the latest years . The 2020 travel season was very low due to the Covid . Notice in the chart 2021, July was also very strong. There were 170,000 jobs added from Travel and Leisure and Hospitality and Dining together. I expect sharply lower numbers in the coming months.

However, to put this in perspective, even taking out a couple hundred thousand out it would be a decent report.

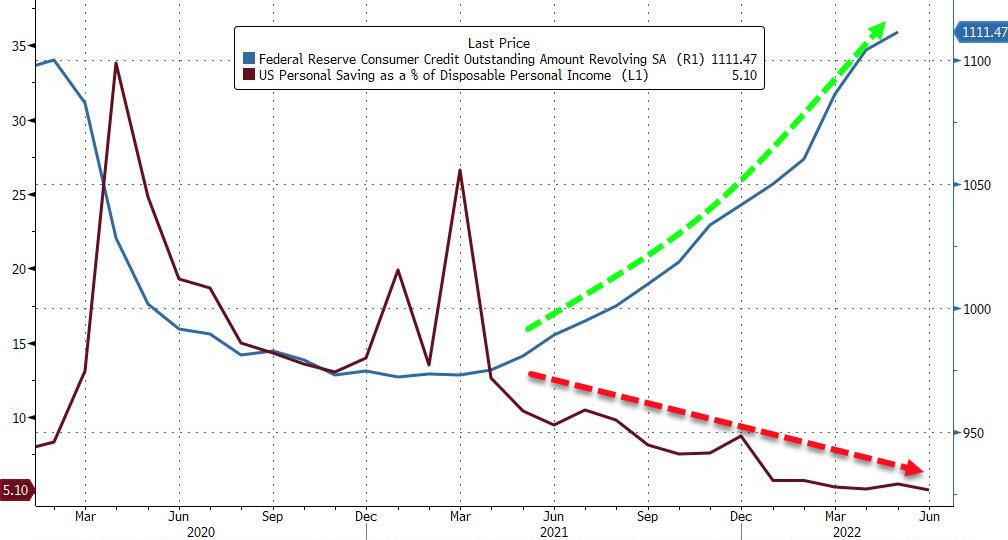

A poor sign came up Friday at 3PM. The June monthly credit increase was $42 billion up from $23 billion. In 2019 about $20 billion was normal.

Most economists write about a lot of money in bank accounts for future spending. This is mainly concentrated in the high end.

Many bankers have said the consumer is still spending. They see it in their credit card data. This is true. However, the consumer is borrowing to do this.

The chart below illustrates the borrowing is suddenly mushrooming significantly above 2019 levels. At the bottom, the savings rate has has fallen below the 2019 level .The trend does not look good for July. It would be great to see the level falls back towards $20 billion a month, but the bankers current data is showing strong spending in July

I have mentioned a concept in another report that YOLO, you only live ounce, is in play this year. The need to get out and vacation is extraordinary. It looks like there is borrowing to do this. I anticipate a decline in spending in the Fall as debt laden consumers slow down.

The big number of the coming week is Wednesday, the CPI!!! The forecasts are for 0.2% m/m compared to 1.3%. The y/y would drop from 8.75 from 9.1%. The Core is expected to rise 0.6% from 0.7% m/m and 6.1% from 5.9.% y/y. This one is more sticky. It is likely we have seen peak CPI inflation, baring a sudden rise in oil.

The Employment Report complicates analysis. Ordinarily I would say the recession could be mild assuming this report being accurate. At the same time it is likely to make the Fed be more hawkish. Core inflation is the most important factor. Rising wages are a key part of embedded broad inflationary psychology.

The World Composite PMI is at the lowest level in two years.

Jun-22 Jul-22

Output 53.5 50.8 Growth, slower rate

New Business 51.4 51.2 Growth, slower rate

New Export Business 49.3 48.0 Decline, faster rate

Future Output* 61.2 60.2 Growth expected, lower optimism

Employment 53.1 52.1 Growth, slower rate

Outstanding Business 50.2 49.2 Decline, from expanding Input

Prices 69.3 67.7 Inflation, slower rate

Output Prices 59.7 58.1 Inflation, slower rate

The economic environment is as complicated as it ever gets. The U S has rising rates into slowing business. EU has massive energy problems and rising rates. The Russian war is widely disruptive. China is trying to stimulate, but being inhibited by its Covid policy.

Jerry